How Citizens Bank used its cooperation under SEDRA to strengthen the way it serves MSME businesses

Nepal’s banks are no longer operating in the easy-growth environment of the previous decade. Loan growth has become more selective, asset quality is watched more closely, and customers have become less patient with slow, paper-heavy banking. For a bank serving MSMEs, this combination creates a difficult but practical question: how to keep lending without simply adding risk.

For Citizens Bank International Limited (CZBIL), this environment created a practical question: how can a bank continue to support MSMEs without simply taking more risk? Over the last three years, CZBIL has cooperated under the Sustainable Economic Development in Rural and Semi-Urban Areas (SEDRA) Phase III program, financed by KfW Development Bank and supported by Business & Finance Consulting GmbH (BFC), a Swiss company with a branch office in Nepal. CZBIL did not approach MSME finance only as a matter of launching new loan products. The work gradually moved into the operating machinery behind those products: how customers are identified, how files are prepared, how risk is assessed, how data is used, and how the bank follows up after disbursement.

The cooperation worked best where external tools met internal ownership. BFC brought methods, templates and an outside view, but the practical test was always inside the bank: whether CZBIL teams could adapt the ideas, use them, and keep improving them after the pilot stage. The bank brought internal commitment, dedicated staff, and regular involvement at the C-level, all of which proved to be decisive. Some initiatives progressed faster than expected, while others required more time, and some were discontinued along the way. The overall direction, however, remained clear: to make MSME banking more structured, more data-driven, and easier for customers to access.

Turning customer data into action

One early lesson from the cooperation was that many opportunities were already inside the bank’s own customer base. Like many banks, CZBIL had a broad deposit portfolio, but not all customers were active. Earlier analysis found many dormant accounts, strong concentration among the biggest depositors and limited segmentation of smaller customers. The issue was not the lack of data. The issue was turning data into useful action.

This led to a deposit mobilization pilot built around customer scoring and targeted outreach, rather than broad, generic campaigns. The results were clearly measurable. Pilot branches achieved deposit growth several times higher than the bank-wide average, with a 17.3% increase in account balances compared to 3.4% across the bank. In addition, more than one third of dormant accounts were reactivated.

This led to a deposit mobilization pilot built around customer scoring and targeted outreach, rather than broad, generic campaigns. The results were clearly measurable. Pilot branches achieved deposit growth several times higher than the bank-wide average, with a 17.3% increase in account balances compared to 3.4% across the bank. In addition, more than one third of dormant accounts were reactivated.

At first, this looks like a deposit-mobilization result. In practice, it also says something important about MSME banking. A bank that understands how customers save, transact and use accounts can serve them better on the lending side as well. For MSMEs, this can mean more relevant offers, more timely contact and a relationship that is based not only on collateral, but also on actual behavior.

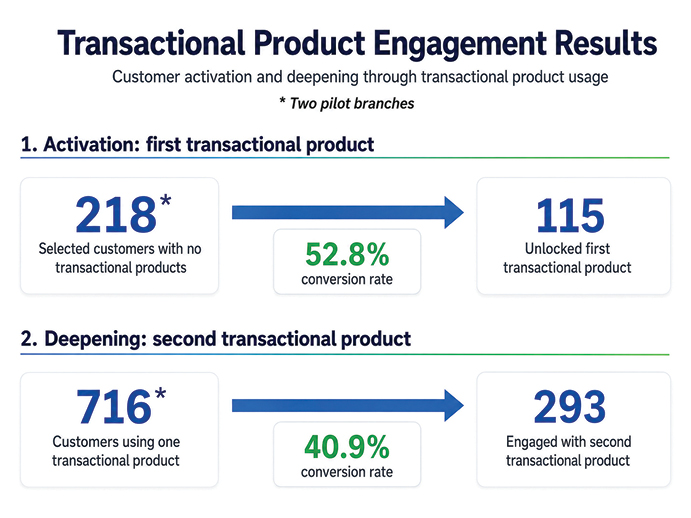

A similar approach was also applied to transaction banking products, as CZBIL aimed to increase the usage and penetration of transactional services. Beyond generating additional fee-based income for the bank, the expansion of transactional banking products also contributes to the broader development of the cashless economy.

The assessment of product co-usage patterns included more than 100 parameters, combined with customer segmentation by demography and occupation, highlighted the need for differentiated sales strategies rather than a standardized, one-size-fits-all approach. Based on these findings, tailored sales and service approaches were proposed for different customer categories.

The results came in quickly and were measurable in clear terms. Conversion rates in those branches went past 50 percent within the pilot period, and mobile banking renewals reached around 80 percent in the same window. In addition, CZBIL discovered a significant pool of customers whose digital banking products had either expired or become inactive without being identified in a timely manner. Reaching out to those customers in a structured way is now a regular part of the branch routine. This has unlocked the value of existing relationship rather than chasing new acquisitions.

Sales as a cross-cutting discipline

Sales as a cross-cutting discipline

The sales management part is often less visible than new products or digital tools, but it has a direct effect on customer experience and business KPIs. MSME clients rarely judge a bank by its internal process design. They judge it by simpler things: whether the requirements are clear, whether someone calls back after the first meeting, how often they are asked for one more document, and how long it takes to get an answer.

Under SEDRA, CZBIL strengthened how it approaches sales and service by looking at the full customer journey rather than isolated elements. This included assessing service quality at branch level and discrepancies across branches, improving how leads are generated and followed up, refining communication with clients, and reviewing the role of digital channels. It also explored a more centralized approach to managing sales activities. None of these changes is dramatic on its own. But MSME banking often improves through exactly this kind of operational discipline: fewer lost leads, clearer follow-up, and less variation between branches.

The cooperation showed that improving sales is not only about assigning targets. It requires better discipline in tracking leads, consistent communication with customers and stronger coordination from head office. This remains a work in progress. Even so, it has already helped shift the conversation from “What growth target should a branch meet?” to “How can we consistently identify, approach, and support the right customers?”

Credit process as the core of change

Credit process as the core of change

The credit workflow optimization became one of the central focal areas of the cooperation, bringing together a set of closely connected changes. Interventions ranged from a more suitable MSME credit analysis approach and expanding collateral-free lending, to reorganizing underwriting through a centralized model. In addition, automation tools such as agricultural technical cards and CIB data parsing plugin were introduced for more rule-based credit appraisal, alongside improvements in process-related data management.

The common thread was simple: CZBIL needed a credit process that could deal with smaller, less formal businesses without relying only on collateral or individual judgement. Serving MSMEs requires a clearer, more structured way to understand them, particularly when financial information is incomplete or informal, and to convert this understanding into efficient decision-making.

The alternative MSME credit analysis methodology aimed to bridge this gap by guiding staff to assess the underlying business, not just the available collateral. It was closely linked to the collateral-free MSME loan pilot under SEDRA and later reinforced through the broader use of CZBIL’s own Citizens Fast Track Loan and QR Merchant Loan, resulting in 225 collateral-free loans totaling NPR 105 million.

The portfolio has remained healthy so far, which is important in a market where collateral-free MSME lending is often easier to discuss than to execute. It also highlights a key lesson: progress requires both ambition and patience, as early disbursements were slower than planned and some ideas had to be postponed due to risk constraints.

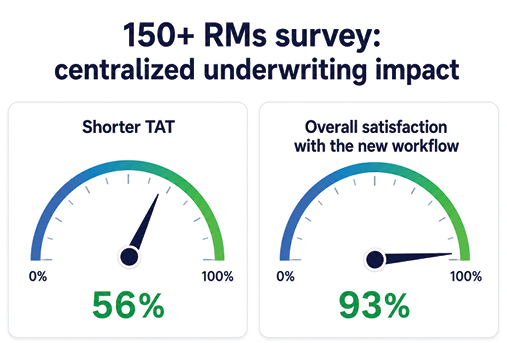

Centralized underwriting added another layer. CZBIL moved toward a model where MSME and retail proposals within defined limits are reviewed faster and more consistently by a dedicated unit.

The aim was not only speed, but also better proposal quality, clearer responsibility and improved management visibility. During the piloting period, BFC helped review workflows, identify gaps in LOS tracking, develop operating procedures and introduce tools for monitoring proposal returns, turnaround time and workload.

The pilot also showed the limits of centralization: delays still start at the branch level before the file reaches the central unit. Some system features also need improvement, for instance tracking of various extended data points. Once the bank resolves these issues, it can identify and manage bottlenecks more directly.

The agricultural technical cards and the CIB plugin contribute to the same broader objective. The agri analysis tool enables staff to assess farming businesses in a fully automated way, with cash flow history and projections calculated automatically based on a large database of real market agronomy and financial benchmarks. The CIB plugin is designed to parse and analyze key credit history information more efficiently and integrate it directly into the loan origination process, without manual RM intervention. Together, these and other tools support a shift toward a credit process that is less dependent on individual practices and more driven by structured, standardized information.

Products that follow behaviour

Products that follow behaviour

Product development also played a key role, but the strongest examples were not products designed in isolation. They were closely linked to customer behavior.

The QR Merchant Loan is the clearest case. As QR payments become part of everyday commerce in Nepal, small merchants leave a useful digital footprint. CZBIL, with BFC support, analyzed QR transaction data and identified more than 1,500 potential customers for a transaction-based, collateral-free loan. The bank then developed and launched the product through a phased approach with pre-approved elements. The process is not yet fully digital, but it has already reduced the need for customers to visit bank premises for approval and disbursement. After the initial 5 months of the pilot, over 150 QR Merchant Loans have been disbursed.

This is a strong example of realistic innovation management. MSME lending cannot become fully digital overnight. Risk checks and customer validation still matter. But it shows how transaction data can gradually improve access to finance for smaller businesses that may not fit traditional collateral-heavy models.

For customers, the value is practical. A merchant actively using QR payments becomes visible to the bank in a new way. The bank can identify demand earlier, reach out more directly, and offer a product linked to actual business activity.

Early recovery and prevention

As asset quality pressure rises across the sector, recovery practices are becoming part of customer-centric banking. This may sound counterintuitive, as recovery is often seen only as pressure on borrowers. In practice, early-stage recovery focuses on timely communication, clear follow-up, and workable solutions before a temporary delay becomes a long-term problem.

Under SEDRA, CZBIL began reviewing its recovery processes and guidelines as part of the broader credit process agenda. Better lending is not only about approval. It also requires consistent monitoring, early warning signals, active customer engagement, and disciplined follow-up after disbursement. A new recovery software module is being developed based on BFC functional requirements.

For the bank, this helps protect portfolio quality. For customers with viable businesses, it creates a chance to address issues early. In the current market, this is part of responsible MSME lending, not an afterthought.

At the same time, discussions addressed root causes of recurring issues, particularly past overreliance on collateral and overly optimistic projections. As these are gradually corrected, RMs are expected to spend less time on recovery, which can currently take up to one month per quarter, similar to most other banks in Nepal, and refocus on their role as revenue-generating front office staff.

Recognition in a broader context

During the cooperation period, CZBIL also received external recognition. The Banker named Citizens Bank International as Bank of the Year for Nepal in 2024 and 2025, highlighting, among other aspects, the bank’s digital initiatives and service development. The bank’s management acknowledged BFC’s support as one of the contributors to its broader operational strengthening.

Such awards should be interpreted with care. They are never the result of one or two initiatives alone, but reflect the wider performance of CZBIL’s management and staff. Still, the timing is relevant: the recognition came during a period when the bank was investing in many of the same capabilities that matter for modern MSME banking.

What it all means for MSME clients

What matters is how changes in the bank’s processes translated into real improvements for customers.

For MSMEs, the impact is practical. Some businesses with limited collateral now have more access to finance and a more structured way to be assessed. Merchants using QR payments can be considered based on transaction behavior. Agricultural clients can be analyzed with tools that better reflect their real business cycle. Loan files can move through a more consistent unbiased underwriting process. Dormant or under-served customers can be approached with more relevant offers.

The practical value for clients is not only easier access to finance, but a banking relationship that is more predictable, better informed and less dependent on collateral alone.

The road ahead

The work is not finished. Some processes are still only partly digital, data gaps remain, and branch discipline will continue to influence the quality of implementation. The shift from collateral-based lending toward stronger repayment capacity assessment will also take time, especially because it requires changes not only in tools, but in everyday habits and mindset across the bank.

This is where the next stage becomes important. For CZBIL, the challenge is less about adding more initiatives and more about making the improved practices routine: using data consistently, reducing case-by-case variation, strengthening risk-based pricing, and keeping the customer experience clear and predictable. That may become a more difficult part of transformation, but also the part that determines whether the changes last.